With summer winding down, the U.S. stock market is set up for a potentially shaky fall.

“Recession fears are the most likely trigger of a retest of the June lows,” said Ed Clissold, chief U.S. strategist at Ned Davis Research, in an Aug. 31 note. “From a seasonality perspective, a retest could come in the next several weeks.”

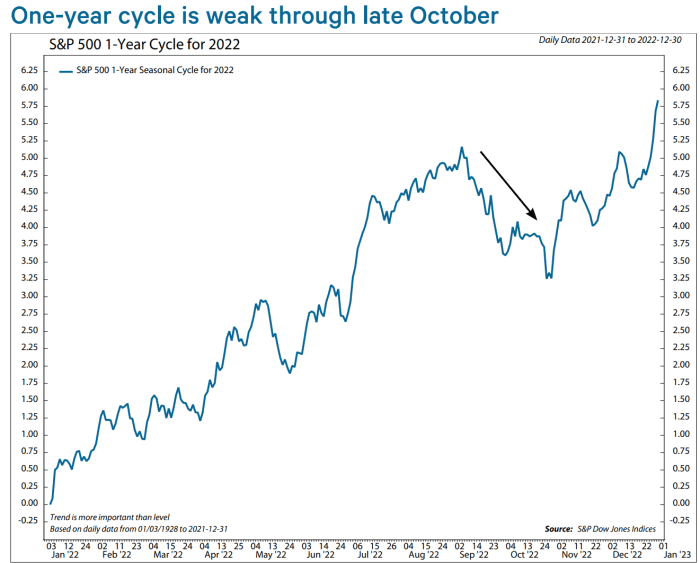

When U.S. investors return from the long Labor-Day weekend, history indicates they’ll be facing the weakest time of the year for the S&P 500 index: the stretch from Sept. 6 to Oct. 25, according to the note.

NED DAVIS RESEARCH REPORT DATED AUG. 31, 2022

The stock market is already wobbly.

U.S. stocks closed sharply lower Friday, with all three major benchmarks suffering a third straight week of losses. Still, the S&P 500

SPX,

ended 7% above its 52-week low of 3666.77 on June 16, according to Dow Jones Market Data.

“I think we have to go back and test that level,” said Bob Doll, chief investment officer of Crossmark Global Investments, in a phone interview. “I don’t think the bear market is necessarily over,” he said, though “what I don’t see is a massive decline from here.”

Read: ‘Prepare for an epic finale’: Jeremy Grantham warns ‘tragedy’ looms as ‘superbubble’ may burst

Meanwhile, ongoing interest rate hikes by the Federal Reserve to combat soaring inflation in a slowing U.S. economy increase odds of a recession along with the prospects of this year’s stock-market lows being retested, according to the Ned Davis note. The Fed this year is “committed to removing liquidity from the financial system,” making a retest more likely, wrote Clissold.

Vanguard Group said in a Sept. 1 report that it downgraded its forecast for U.S. economic growth this year after two straight quarters of contraction. The firm now expects economic growth of 0.25%–0.75% for full-year 2022, down from its estimate last month of about 1.5%.

“We believe it likely that the United States will struggle to regain above-trend growth in the quarters ahead,” Vanguard said. “We place the likelihood of a U.S. recession at about 25% in the next 12 months and 65% in the next 24 months.”

Whether any “retest” of the stock market’s lows is brief may depend on the ability of the U.S. to avoid a recession, according to Ned Davis.

“The average non-recession bear lasts about seven months and has declined 25% (-18% over the past half century), putting the January – June drop in line with the typical case,” Clissold wrote in the Ned Davis note. “Conversely, the average recession bear has lasted about a year (17 months over the past 50 years) and declined a mean of 35%.”

Inflation ‘dragon’

Investors have been anticipating another large interest rate hike from the Fed at its Sept. 20-21 meeting, after chair Jerome Powell sent a clear message in his Jackson Hole speech on Aug. 26 that the central bank would keep battling high inflation until the job was done – even if that means some pain for households and businesses.

Stocks swooned on his remarks that day, with the Dow Jones Industrial Average

DJIA,

closing down 1,000 points and losses have deepened since then.

The “vigorous” rally in stocks seen earlier over the summer had reflected “too much optimism given we’re still in the early stages of fighting inflation,” said Crossmark’s Doll. Although he thinks inflation has peaked, Doll predicts that its continued decline this year will likely be irregular and finish 2022 above the Fed’s 2% target.

“It’s not going to end up at a level where we say, ‘ok we got that dragon, what’s next’?” he said. If inflation, which ran as hot as 9.1% in June based on the consumer-price index, comes down to 4% or 5%, “that’s good news, but it’s not enough good news to say the Fed’s done,” said Doll.

Vanguard expects the Fed to increase its federal funds rate target to a range of 3.25%–3.75% by year-end, from near zero at the start of 2022, according to its note. That compares with a current range of 2.25% to 2.5%.

Ahead of Powell’s Jackson Hole speech, the market narrative had switched away from the Fed fighting inflation through aggressive rate hikes to, “when are they going to pivot?” said Steve Sosnick, chief strategist at Interactive Brokers. But using a relatively short speech, which had “no ambiguity,” Powell turned the focus back to monetary tightening and the Fed’s unfinished fight with inflation, sending “a very powerful message to the market,” said Sosnick.

“We’ve been dealing with that ever since,” he said, pointing to stock market losses.

“The fact that we’ve moved so far so fast, and the psychology has changed so quickly, makes me think that we are nowhere near seeing the last of volatility, particularly into the fall,” said Sosnick. “The September-October period definitely gets more than its share of market weirdness.”

Stock-market bottom?

Equity and quant strategists at Bank of America said in a BofA Global Research note dated Sept. 2 that valuations for the S&P 500 remain “rich.” In their view, “a bottom is not in.”

“Initially, the rally off the June lows looked more like a young cyclical bull than a bear market rally,” said Clissold, in the Ned Davis note. “Several breadth thrusts and expanding new highs suggested much of the decline had run its course.”

But intermediate-term and long-term breadth needed to follow to confirm a bull market, he said, and without that confirmation, “a retest cannot be ruled out.”

“The S&P 500 stalled just below its falling 200-day moving average and has given up about half of its June 16 – August 16 gains,” Clissold wrote. Also, “the percentage of stocks above their 50-day moving averages just missed its 90% threshold.”

U.S. stocks ended Friday with weekly losses, with the S&P 500

SPX,

shedding 3.3% while the Dow Jones Industrial Average

DJIA,

fell 3% and the technology-heavy Nasdaq Composite

COMP,

dropped 4.2%.

The U.S. stock market will take a break on Monday to celebrate Labor Day, resuming trading on Tuesday. The economic calendar for the upcoming week includes data on U.S. services, jobless claims and consumer credit, as well as the release of the Fed’s “beige book,” which includes a collection of business anecdotes from around the country.

The Fed’s continuation of aggressive rate hikes combined with weakness ahead for company earnings and the labor market “is not a strong backdrop for the equity market,” said Liz Ann Sonders, chief investment strategist at Charles Schwab, by phone. Also, “we know September, seasonally, tends to be a weak month” for stocks.

| Hollywood.com Movie Trailers")