Jump To:

What Is BNPL? | The History of BNPL | The Consequences of BNPL | The Future of BNPL

Oberon Copeland, a consumer products reviewer, had been using buy now, pay later (BNPL) services for a few years without a hitch to buy various items online. A pair of shoes. A new mattress.

One one hand, “BNPL services were a lifesaver, as I was furnishing a new apartment and did not have disposable cash at the ready,” he says.

On the other hand?

“I’ve also gotten myself into some financial trouble by using them too impulsively,” he says.

Copeland recently used a BNPL service to buy a new TV, then ran into financial difficulties, missed a payment had to swallow a late fee.

“This experience has taught me to be more careful with my spending and make sure I will be able to cover the balance when it’s due,” he says.

Meanwhile, Jennifer Darnell — blogger, traveler and mom of four — says she uses BNPL services to strategically book her family’s flights.

“I often cannot come up with a large sum at once, or would have to save for months, then plan the trip,” she says.

Using a BNPL service let her take advantage of a Southwest 40% off sale right when it hit, save $400 on her family’s flights and then pay off the trip (interest free) over time.

“By the time our trip comes up, my payments will be complete, and my trip will be paid for,” Darnell says.

These two stories show two paths BNPL can lead consumers down. One leads to a shopping holy grail: The stuff you want and the ability to get it, despite not having the funds yet. But the other path can be a bit more winding.

With inflation at historic highs, BNPL services (Klarna, Zip, Afterpay, Affirm, et al.), which let you pay for goods interest free over multiple payments, are compelling to many consumers. Plus, the quick approval process makes using these services less onerous than applying for traditional forms of credit, like credit cards.

The low-stakes feel and ease of BNPL is as hard to ignore as the services themselves (if you’ve shopped online at any point in the past two years, you’ve seen them waiting for you at checkout).

But, like all financial products that let you get stuff with funds that aren’t quite in the bank account yet, there are risks in addition to the rewards. What happens, for example, if the money you were certain would be in your account by the time payment comes due doesn’t materialize? Or needs to be spent on something more pressing? What does it mean for your credit score and financial health?

“The reality is, a lot of the people who are jumping in and using [BNPL] don’t really understand it,” says Howard Dvorkin, personal finance expert, chairman of Debt.com and previous president of the Association of Independent Consumer Credit Counseling Agencies.

Consumers, consumer advocates and the credit bureaus are all contending with this relatively new, rapidly growing financial service and its impact on the consumer borrowing world in real time. Here’s what shoppers need to know before checking out with BNPL.

What Is BNPL?

There are currently dozens of BNPL services in the U.S. (Affirm, Klarna and Afterpay being the big three). And they all function a bit differently. The one you use will depend on which service(s) a store partners with.

But what they all have in common is this: They allow customers to quickly get a line of credit at online checkout to cover a purchase and then pay that purchase off over time (usually six to eight weeks) without paying interest. Whatever you buy ships immediately, even though you haven’t paid it off. In addition to being usable online, BNPL is developing an in-store presence. Just install the app of your BNPL service of choice and get a barcode to scan in person at a store that partners with that service.

The interest-free part is what makes BNPL unique from credit cards, which generally require you to pay interest if you carry a balance past a month. And the ability to get a product immediately makes BNPL different from layaway, which requires payment in full before you take the product home.

BNPL services make money through a combination of late fees and other various fees they charge the merchants they partner with, which want to attract shoppers who wouldn’t be able to shop them otherwise. Some retailers also pay to have their deals promoted in BNPL providers’ apps. Some BNPL services have also launched other financial services, including debit cards (which means they make money via interchange fees) and longer-term loans that actually do charge interest.

A Short History, but a Growing Presence

Most BNPL companies active in the U.S. began in Australia and Europe. Seemingly overnight, they’ve become omnipresent at online checkouts. Here are a few key moments in history:

- 2015: Klarna starts testing in the U.S. and makes CNBC’s Disruptor 50 list in 2016.

- 2018: Afterpay starts operations in the U.S.

- 2019: Walmart announces it will be using Affirm as its pay-over-time provider and ditches its traditional layaway program.

- 2021: American financial services and payments company Square announces it’s acquiring the Australian BNPL company Afterpay.

- 2022: Amazon announces that it will be integrating Affirm into Prime Day, allowing shoppers to pay off Prime Day purchases of $50 or more in three interest-free payments.

- 2022: Apple announces its own in-house BNPL program, called Apple Pay Later.

User numbers also show that BNPL has quickly become a mainstream financial product. According to June 2022 numbers from research firm eMarketer, Klarna comes in first at about 35 million U.S. users, Afterpay in second at 20 million and Affirm in third with about 14 million.

BNPL doesn’t have nearly the footprint credit cards do — at least not yet. According to eMarketer, a little more than one-third of shoppers in the U.S. will use BNPL in 2022, which means BNPL is still dwarfed by credit cards: 79% of U.S. consumers use credit cards (according to 2021 numbers from CreditCards.com), and there are about 200 million credit cardholders in the U.S.

But BNPL is growing. Affirm confirmed with us that their active users are up 137% from the year before. And, according to a January 2022 survey performed by RetailMeNot, 23% of shoppers said they had used BNPL in the past 12 months, while 32% said they planned to use it in the coming year.

The Consequences of BNPL: The Good, the Bad and the … TBD

So, BNPL is very much here. It’s very much growing. And it’s very convenient. Is that good or bad? Depends on who you ask — and from what angle you’re considering this still-relatively-new kid on the payments block.

1. The Approval Process Is Quick and Painless

BNPL services are a seamless way to shop and acquire credit, all in one go. And the hurdle to qualify is generally lower compared to other forms of credit.

“Unlike applying for a new credit card, BNPLs are easier to qualify for,” says Katie Bossler, quality assurance specialist at GreenPath Financial Wellness, a nonprofit credit counseling organization. “This means that someone who is new to credit or doesn’t have a strong credit profile might find it more appealing to make a purchase this way.”

Take credit cards for example. Even if you simply want to finance a $100 coat, you’d first have to get a card. That means applying to prove you are worthy of a credit limit that you won’t know until you’re approved (often thousands of dollars). With BNPL, you can apply right at checkout to get approved for just enough to cover your purchase.

And then, there’s the approval process, aka the “credit pull.” In the credit world, a soft pull is generally used by lenders to prequalify potential borrowers and verify identity, while a hard pull occurs when you seek out and apply for credit. The former does not affect your credit scores (including your FICO scores), while the latter dings your credit scores.

BNPL providers generally don’t use the hard pull protocol — traditional plastic and loans do. Instead, BNPL providers use the soft pull protocol (for their short-term installment point-of-sale products), or verify your identity and credit history in other ways (including your past behavior with their services). That means you can usually apply for a BNPL loan (or several BNPL loans) without a single credit ding.

In other words, applying for a BNPL loan is a relatively quick process that won’t dent your credit score up front.

That doesn’t mean BNPL providers have no underwriting process, though.

We reached out to Klarna, Afterpay and Affirm to ask about the guardrails they have in place. While none agreed to have a named spokesperson on the record, all responded to emails and questions from RetailMeNot and provided the following information regarding their underwriting:

Klarna

- Klarna conducts “eligibility requirements” and an underwriting process for each purchase to get a “real-time view of someone’s financial circumstances,” a Klarna spokesperson wrote us. Klarna also uses other datapoints, including the borrower’s history of using Klarna in the past, and the spokesperson emphasized, “Using Klarna is never guaranteed, even for returning customers.”

- If you continue to use Klarna to finance multiple purchases, spending limits are flexible and factor in data like repayment history with Klarna, your outstanding balance and more. The initial approval might be enough to cover a small purchase, but those who show good repayment history will get more purchasing power. Meanwhile, use of Klarna might be restricted if someone misses payments.

Afterpay

- Afterpay, its spokesperson says, starts overall purchase borrowing limits low and increases them over time with positive payment history.

- A single late payment freezes a consumer’s ability to make new purchases with Afterpay.

- According Afterpay’s spokesperson, a study commissioned by Afterpay shows Afterpay users are as half as likely to be delinquent than credit card users.

Affirm

- Affirm uses an underwriting model that takes into account a person’s transaction history with Affirm and credit usage. It uses machine learning to calibrate its underwriting, its spokesperson wrote us.

- Affirm’s spokesperson emphasizes BNPL’s ability to approve or deny someone at the transaction level, rather than (like credit card issuers) extending a large open-ended line of credit.

- Incomplete or late payments can get someone cut off from future Affirm loans.

All three emphasized they also offer hardship policies and the ability to defer payments temporarily.

2. Interest-Free Repayment Can Be a Tempting Financial Snooze Button

“Consumers may buy now and think later about payments and not plan those payments within their budget.”

Katie BossleR, GreenPath Financial Wellness

Easy approval aside, the thing that BNPL is perhaps the most famous for is interest-free repayment. But, while not having looming interest charges is enticing, whatever you borrow with BNPL services needs to be repaid, just as it would be if you’d put it on a credit card.

“No interest, pay it over a couple months? That sounds great,” Dvorkin of Debt.com says. “What happens if you go on a shopping spree? All of a sudden, you rack up a couple thousand dollars in one day, one hour. And then you have to face it next month. You may buy more because it’s so easy.”

This smoothing out of the traditional hurdles of shopping and borrowing might make shoppers less critical of their purchases, Bossler agrees.

“Consumers may buy now and think later about payments and not plan those payments within their budget,” she says. “Consumers tend to spend more and increase impulse buying with BNPL options.”

And no matter how cautious BNPL services are or aren’t in their underwriting and approval process, one thing that gets consumers into trouble is the sheer number of BNPL services out there, Dvorkin points out. BNPL services don’t consistently report past payment history to each other. A bank pulling credit reports can see how underwater a person is with other credit cards and loans. But one BNPL service, for example, can’t see if someone is underwater with another. So a person could conceivably check out with several BNPL loans in rapid succession and get overextended before their accounts get frozen.

“The problem is, when you’re juggling multiple buy now, pay later accounts, you might get yourself in trouble,” Dvorkin says. “I’m a CPA. I don’t miss much. But you get five, six of these things floating around a month, you’re going to miss one. It’s not surprising. Then it leads to collection action.”

3. Unpaid BNPL Balances Have Consequences, Including Credit Damage

That “collection action” Dvorkin mentions is the crux of BNPL’s risk to your credit, albeit a delayed one. The services advertise “no credit damage” in their marketing, in reference to the fact that they don’t conduct a hard pull on your credit up front. But, if you really do not pay off your account EVER, the consequences are usually the same as any debt you don’t pay off.

“If you default, it’s given to a collection agency, it’s going to affect your FICO score,” Dvorkin says.

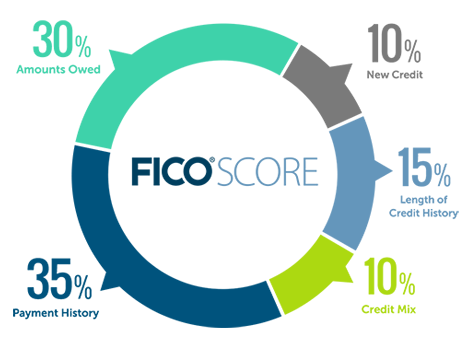

Collection accounts stay on your credit report for about seven years. Those reports feed your credit scores, including your all-important FICO score. In fact, they feed into the “payment history” portion of FICO’s model, which makes up 35% (the greatest portion) of your score. Suffice it to say you do not want collection accounts in your credit history.

The various BNPL services all have different debt charge-off policies and late-payment penalties. Afterpay, for example, says it does not hand over debt to collections agencies, period (it just cuts you off). But others say in their legal paperwork (and confirmed with us via email) that they might charge off your debts after a certain length of time.

| Klarna Pay in 4 | Afterpay | Affirm Pay in 4 | |

| Upfront payment | 25% | 25% | Varies |

| Length | 6 weeks (pay every 2 weeks) | 6 weeks (pay every 2 weeks) | 6-8 weeks (pay every 2 weeks) |

| Late-payment fee | $7 (up to 25% of order value) | $8 (up to 25% of order value + account paused) | None |

| Debt collection policy (if you don’t pay) | May employ a debt collection agency to collect on default accounts without payments for multiple weeks. No additional fees, bailiffs or legal action. |

None. But may terminate your access to Afterpay. | Charge-off possible after 120 days of nonpayment. |

For some borrowers, though, the nebulous, delayed threat of possible collection actions (and credit report damage) isn’t enough to dissuade them from overusing BNPL services. In fact, many BNPL users may already have collections accounts in their credit history — and use BNPL as a way to buy things when they don’t otherwise qualify for credit cards.

“So they don’t care,” Dvorkin says. “‘My credit’s already bad,’ they’re thinking.”

After all, it’s not like a buy now, pay later company is going to repossess that TV you bought.

“There are very few consequences,” Dvorkin says. “They don’t charge interest. And they don’t chase you. Their collection systems aren’t developed enough to chase you down.”

In fact, all the BNPL providers we contacted say they do not engage in aggressive debt collection practices.

- Klarna says it uses debt collection agencies only if repayments are weeks overdue and the user isn’t responding to attempts to contact. “Even at this point, we retain full control over the debt, which means debt collection agencies can’t charge customers any additional fees behind the amount owed, and we specifically instruct them they can’t use bailiffs, initiate litigation or legal action against anyone,” Klarna’s spokesperson wrote us.

- AfterPay brings in third-party debt collectors only after 120 days of nonpayment. Its spokesperson wrote us: “Our third party collectors are required to treat Affirm consumers with the same level of respect and quality of service that we maintain for ourselves. Affirm maintains oversight over its third-party collectors to ensure they meet our high standards of consumer care and compliance. This includes review and approval of consumer communication.”

- Affirm doesn’t hand off debt to collectors at all, but suspends use of its services for those in default.

4. You Can’t Build Good Credit With BNPL … At Least Not Yet

Say you handle your BNPL accounts impeccably and never miss a payment. There’s another issue to consider with BNPL credit reporting — rather, the lack thereof.

“It’s not building up your credit,” Dvorkin says.

That’s because, unlike traditional credit products, most buy now, pay later services don’t report regular payment history to the three major credit bureaus (Equifax, Experian and TransUnion). Those are the Big 3 bureaus that factor into FICO scores. So, even if you behave angelically with your BNPL loans, paying them off on time, you’re not helping your credit score because that good behavior isn’t ending up on your credit reports. Some BNPL services report to alternative bureaus and are factored into alternative credit scoring models – but probably not the reports a future mainstream auto lender or mortgage lender is going to look at.

But you just want to get a new coat. Why do you care if a future lender can see if you paid it off on time?

In the credit world, having no credit history can get you denied, just like having a bad credit history would.

If you have other forms of credit on your credit reports (credit cards or other loans), FICO can get a read on you. But if you’re relying on BNPL to finance all your purchases, you’re not helping your credit score out. And many BNPL users are young; 28% of their user base is under 25, according to eMarketer, and one-third are between 18 and 30, according to Debt.com research, Dvorkin says.

“And that age group only makes up 17% of credit usage,” he says.

So, if you’re young and just building your credit history, don’t expect BNPL to build up the score you need to qualify for a future car loan or mortgage.

“They’re going to start reporting this stuff. You have hundreds of millions of dollars of buy now, pay later loans out there.”

Howard Dvorkin, Debt.com

This is all likely changing though – and soon. Credit bureaus want to (and need to) find a way to factor in BNPL data. Lenders (which pay the credit bureaus for credit reports and scores) want to know potential borrowers’ full financial picture and expect the bureaus to deliver it. They do not want to make decisions based on the tip of someone’s credit iceberg with thousands of dollars of BNPL transactions hiding below the surface.

“They’re going to start reporting this stuff,” Dvorkin says. “You have hundreds of millions of dollars of buy now, pay later loans out there. It’s a massive bucket of information they should be reporting. And credit bureaus have to stay relevant.”

Here’s the current status of BNPL and credit reporting:

- TransUnion is introducing a plan to include BNPL in its reports. Entities that use its data will be able to opt in to receive BNPL data in addition to more traditional data. It’s also working to ensure the “quick” aspect of these loans doesn’t hurt consumers (because, with most credit scoring models, including FICO, opening up several lines of credit quickly can hurt you).

- Experian has created a new BNPL bureau. In its announcement, it emphasized that this will allow consumers with thin credit files to get a leg up with good BNPL behavior.

- In Dec. 2021, Equifax announced it is adding BNPL data to reports, giving BNPL services the option to start reporting data in early 2022. They also did a study and found that those with good behavior on a BNPL account could expect a FICO score increase of 13 points (21 points for new credit users with thin files). Score providers (like FICO) aren’t incorporating this data yet. But lenders using Equifax’s data can opt to have a BNPL tradeline that identifies BNPL loans separately from more traditional forms of credit. Learn more.

Once BNPL data points become a standard fixture on your credit reports, they’ll become part of your credit scores, for better or worse.

“Like credit cards, BNPL plans can encourage discretionary spending and the risk of overspending,” Bossler says. “Like credit cards, they require one to use credit responsibly.”

5. An Economic Downturn Could Spell Trouble for Power-Users

Even if you get to keep the TV you never paid off, even if you’re not worried about your credit now, BNPL is part of your overall financial health and ALL of the forms of credit you are using … or over-using. It’s all connected.

Caroline Tanis, CDFA, of Tanis Financial group, has noticed BNPL loans having a domino effect for her clients.

“They will come to me and have large amounts of credit card debt that they need to pay off,” she says. “And when I ask how they racked up so much debt they tell a similar story about how they used buy now, pay later services and then put those on their credit card, which also delays their payments. Most of the time they can’t figure out what product they spent the money with and forgot they made the purchase, so they just keep piling up on their cards.”

With inflation spiraling and a potential economic downturn looming, Bossler is also concerned about the load some borrowers are carrying.

“We have seen that credit card debt has increased, largely due to inflation,” she says. “Stimulus and similar resources have subsided, consumers are putting large discretionary purchases and services, like travel, on credit cards. The use of BNPL tools for purchases will likely follow this trend.”

The Future of Buy Now, Pay Later

When it comes to financial products, there are risks on both sides. Risks to those who borrow and risks to those who lend. And, with a financial product as new as BNPL, both parties are figuring out how to balance that risk on the fly.

For Dvorkin’s part, he anticipates BNPL providers running into snags with repayment as they grow aggressively. Debt.com’s research indicates that 43% of BNPL users have subprime (aka bad) credit (compared to 13% of overall credit users).

“That’s a big problem,” he says. “A significant amount of people utilizing these have had credit problems in the past.”

“Going down the credit spectrum,” he predicts, combined with the fact that BNPL services aren’t doing a lot to collect on debt, may mean a lot of loans that likely won’t get repaid.

“People are getting themselves in trouble,” he says. “They’re going to build up a ton of these. And they’re not going to be able to pay it back. And the companies that are out there won’t be in business five years from now.”

“People are getting themselves in trouble. They’re going to build up a ton of these.”

Howard dvorkin, debt.com

Trade publication Business of Fashion similarly predicted in July 2022 that the BNPL industry will have to evolve beyond the high-volume of low value (i.e., “$10 T-shirt”-type) transactions, if it wants to stay afloat.

The BNPL industry is also attracting attention from government regulators. Federal consumer watchdog agency the Consumer Financial Protection Bureau (CFPB) has been looking into BNPL loans since December 2021. The CFPB’s most famous consumer-borrowing regulation was the 2009 CARD Act, landmark legislation that put stricter consumer-protection rules in place for the credit card industry.

Nothing like that is in the works for BNPL so far, but the agency is soliciting comments from consumers, consumer advocates, financial institutions and more. It’s also looking into BNPL’s targeting of young consumers and its data harvesting practices.

As for the BNPL companies? We asked them where they see themselves in the future, and they see point-of-service loans as just the beginning of their forays into financial products – and even rewards programs.

- Klarna is offering longer-term financing for bigger ticket items (with interest), as well as a Klarna Card which can be used like a debit card at any retailer, regardless of partnership with Klarna.

Klarna’s spokesperson also emphasized that the company sees its place in the borrowing ecosystem as a safe harbor from credit cards’ interest fees due to its adaptive credit limits. “If people show they can spend and repay responsibly, more will be released next time which is a much more sustainable model compared to credit cards with a high credit limit.”

- Afterpay says it is focusing on offering merchants advertising opportunities to attract its Gen Z and millennial audience of young consumers and is also emphasizing its pay-in-stores option. It also has a deals portal.

- Affirm has a debit card (Debit+), the first U.S. debit card with pay-over-time functionality. It also offers free high-yield savings accounts.

No matter what the future of BNPL looks like, it will likely be shaped by whatever reality takes hold in the next couple years. Will inflation and (possible) recession draw more shoppers into the BNPL fold as access to traditional credit dries up? Will delinquencies push BNPL companies into stricter underwriting and make it tougher for some of its power users to gain access to their entry-level products? Will legit credit reporting of BNPL loans give young borrowers a leg up to good credit? Or will economic strife lead to even more damaged credit histories when BNPL nonpayment data starts flowing onto credit reports?

Our advice to shoppers? Before you buy now, think of the “later.”

The post Buy Now, Pay Later: How Easy Money Can Get Kind of Complicated appeared first on The Real Deal by RetailMeNot.

| Hollywood.com Movie Trailers")